The Insolvency Service has just released its Creditors’ Voluntary Liquidation (CVL) Research Report. The purpose of this report was to ascertain whether the recent reforms in 2017 on the CVL process had, in fact, made the process more efficient and increased the returns to creditors.

Analysis was performed on a randomly sampled dataset of 2,717 completed CVLs which started in 2017.

Efficiency was assessed through three quantitative measures: time to complete the CVL, associated costs, and recovery rates for creditors.

Time: 6% of the sampled cases were ongoing at the time of data collection. The median duration to complete a CVL was 712 days.

Cost: The median cost, represented as fees relative to the estate’s value, was 163%.

Recovery Rate: The median recovery rate for all creditors was 0%, indicating that in many cases, creditors did not receive any return.

One might ask why the median was used, as opposed to the mean, in these calculations. This is mainly because in the random sample there may well be some very large company liquidations that would distort the statistics.

Other interesting statistics that come out of the research are as follows

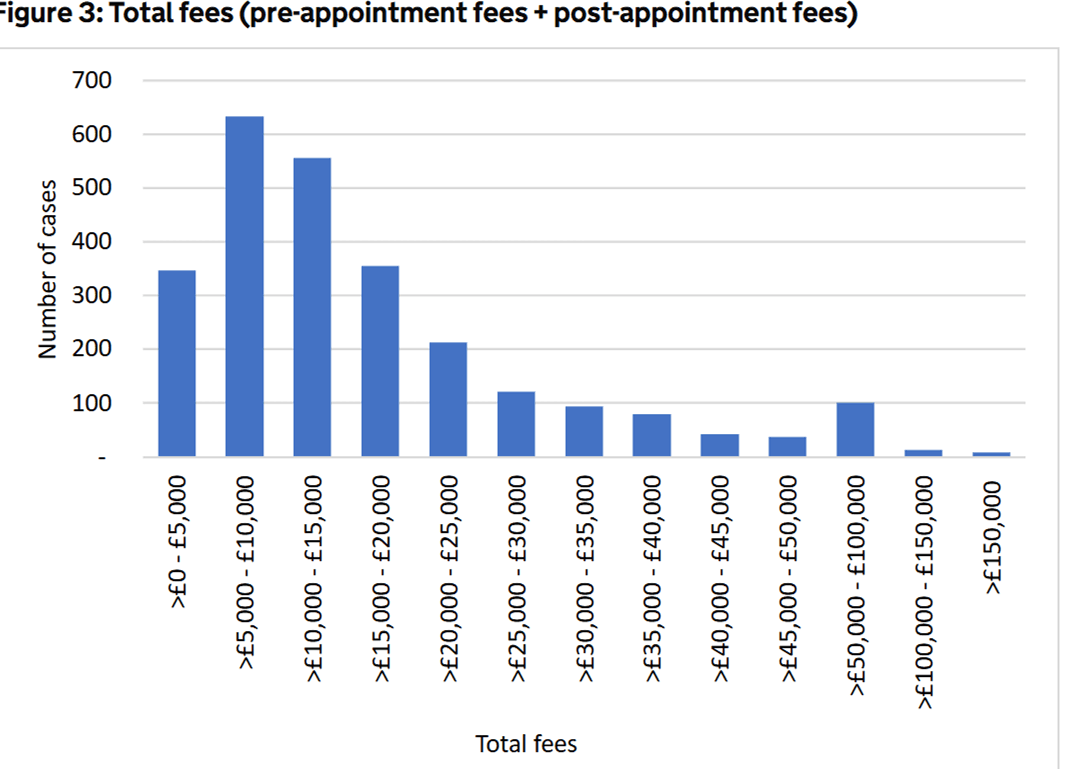

Median Pre appointment fees were £4000 see the chart below that shows total fees.

%27%20fill-opacity%3D%27.5%27%3E%3Cellipse%20fill%3D%22%23cac8d1%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(395.67664%20347.03148%20-146.46916%20167.00048%20208.9%20240.4)%22%2F%3E%3Cellipse%20fill%3D%22%23fff%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(364.97726%206.68966%20-3.68002%20200.77586%20891%20199.7)%22%2F%3E%3Cellipse%20fill%3D%22%23a89bee%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(69.08942%2096.13095%20-77.08235%2055.39917%20278.2%20318.4)%22%2F%3E%3Cellipse%20fill%3D%22%23fff%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(1076.78913%2065.33762%20-6.61536%20109.02367%20558%20709.3)%22%2F%3E%3C%2Fg%3E%3C%2Fsvg%3E)

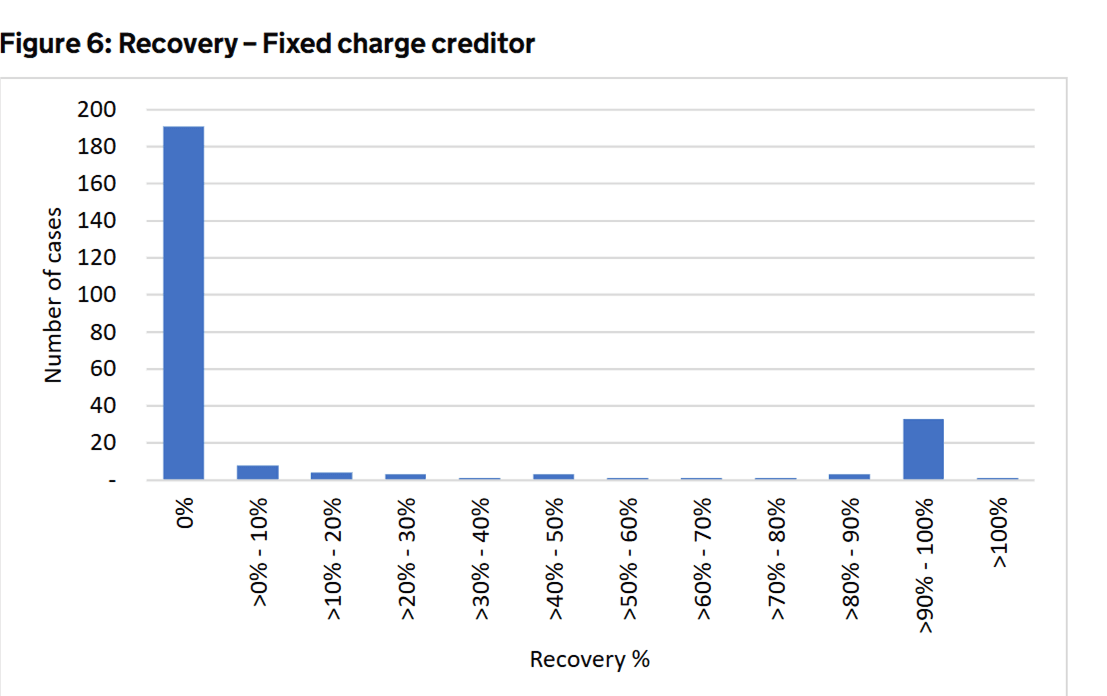

The overall returns to creditors are very poor. The charts below shows preferential creditors that in most cases will be employees and HMRC (post 2020) and Fixed charge creditors who are in fact the first in line showing virtually nil return %27%20fill-opacity%3D%27.5%27%3E%3Cellipse%20fill%3D%22%23cacaca%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(47.90855%20370.51214%20-181.18341%2023.42767%20102.7%20103)%22%2F%3E%3Cellipse%20fill%3D%22%23fff%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(-24.81214%20667.75785%20-477.02552%20-17.72503%20739.8%20278.7)%22%2F%3E%3Cpath%20fill%3D%22%23c9c9c9%22%20fill-opacity%3D%22.5%22%20d%3D%22M387-23.8L287.6%2093%20270.3-28.1z%22%2F%3E%3Cellipse%20fill%3D%22%23fff%22%20fill-opacity%3D%22.5%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(-532.90381%20965.3536%20-608.13099%20-335.70634%20901.1%20689.7)%22%2F%3E%3C%2Fg%3E%3C%2Fsvg%3E)

This poor level of return is concerning as one of the liquidator’s jobs is to try and liquidate the assets to repay creditors. However, remember the company in question has gone into liquidation as it is unable to pay its creditors! Most directors will try and put off the inevitable and borrow against any assets they may have or sell them before they enter liquidation. The reality is that most companies do not have any liquid assets that can be easily sold to repay creditors. Often assets of any value are costly to move or have a limited market value. In addition, the liquidators have to do an investigation into the directors conduct to see if they should be disqualified. In addition, in the name of transparency, they have a duty to keep the creditors informed of the reasons for failure, and why they are not going to get any return.

So, if CVLs offer such low returns to creditors there should be an alternative process that insolvency practitioners should be using and directors should be made aware of!

Administrations are costly and mainly for larger businesses. The alternative is of course the use of more informal deals with creditors such as Time to Pay Arrangements (TTPs) and the use of the Company Voluntary Arrangement (CVAs) insolvency rescue mechanism. These are harder to implement than simply advising the company to liquidate and of course there must be an underlying profitable business there. But surely there are companies out there that could pay off some of the debts over a time period of say, 3-5 years. Even if the CVA or TTP lasts only a year or two it is signicantly better than a CVL that on this research gives Nil return to any creditor! Remember a CVA doesn’t even bind the fixed charge (secured creditor).

The number of TTPs are not really recorded as there is no formal insolvency but the number of CVAs are and it is very low at some 15 or 20 a month.

As a small firm that does the second highest number of CVAs, after Begbies Traynor who are the largest insolvency firm in the UK, we believe they are ridiculously underused.

However using CVAs KSA Group has;

- Distributed £31m to creditors 2009-2022. This excludes secured debts and secured factoring facilities, much of which have been or will be repaid.

- Repaid £17.9m to HMRC between 2009 and 2023, remember this for the most part when HMRC was an unsecured creditor (2009-2020). That’s taxpayers money.

- Saved creditors money.

- Preserved 320 customers for thousands for suppliers, accountants and professional advisors.

Ultimately, the main thing that should come out of this research is that Directors should act early and not bury their heads in the sand. Also insolvency pratitioners should not be afraid of exploring other options for distressed businesses such as TTPs or CVAs.